Reliance Growth Fund – SIP Review and Analysis

Till now we have been only recommending HDFC Funds – Equity and Top 200. However, last month we recommended investors to invest in the NFO of Reliance Long Term Equity Fund. Our research team has carefully analysed Reliance Growth fund managed by Sunil Singhania and we recommend SIP investors to invest in the same.

Reliance Growth fund is a pure equity fund which mainly invests in Large Cap and Mid Cap stocks. If you have seen the presentation of Singhania, you will be convinced that he is in lookout for a sunrise sector and emerging companies of the same. These companies will always give higher percentage of returns.

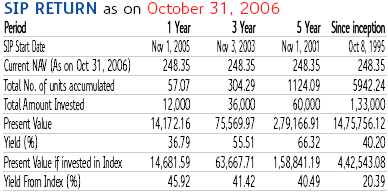

Here is a quick look at historical performance of Reliance Growth Fund. Since inception, it has yielded a compounded return of 33.7% for NFO investors and 40.20% for SIP investors. Your investment of Rs 1,33,000 over a period of 11 years is today worth, Rs 14,75,756 🙂 Kindly take a look at the attached excerpt from the latest factsheet.