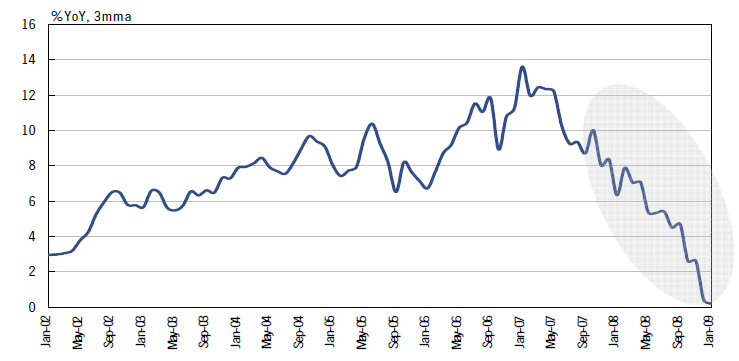

Industrial production declined 0.5% YoY in January-09 compared with a decline of 0.6% in December-08 (revised upwards from -2% earlier) and growth of 1.7% in November. The decline in January was lesser than market expectations (Bloomberg survey) of -0.9%.

The manufacturing segment declined 0.8% in January compared to -1% in the previous month. The key contributors to this decline were food products, non metallic mineral products, basic metal & alloy industries and metal products & parts. The mining segment also declined 0.4% in January compared to growth of 1.8% in the previous month. The growth in the electricity segment, however, accelerated to 1.8% vs. 1.6% in December.

Growth in consumer goods decelerated to 1.1% in January compared to 1.5% in December. Within consumer goods, growth in the durables segment accelerated to 2.5% on low base effect (vs. -4.1% in December) while non-durables segment growth slowed to 0.7% vs. 3% in December. Capital goods growth accelerated to 15.4% in January mainly on low base effect compared to 5.2% in the previous month. Basic and intermediate goods declined 1% and 9.2% in January (vs. +1.9% and -9.4% in December) .

Other indicators of activity such as the Purchasing Managers Index, exports growth, non-oil imports, and motor vehicle sales have also been very weak in January. We continue to expect activity to slow considerably in the January-March quarter of FY09.

In a related development, Indian Inflation Touched a new 6 year low at 2.43%.