In a report Morgan Stanley disagrees with the current rally in the Indian market. It appears that investors are starting to build a bull case for India. In agreement with India’s long-term story is intact but we do not see a reason to buy Indian equities at least until the elections. Recently developments in politics seem to be increasing the probability of very fragmented parliament, which could spoil chances for a post election recovery in markets as well with a likely downgrade of sovereign rating. (more…)

Author: CP

Real Estate Companies still in a Risky Business Model

In the present credit crunch, investors seem to be more concerned about pressure on corporate balance sheets than on earnings. BNP Paribas has done an excellent research to estimate the risk to companies’ debt servicing capabilities and the risk to companies’ capex targets under various scenarios of revenue and cash flow decline (5% to 30% decline) from base case estimates.

Naturally, a company that faces risk to debt servicing under a scenario of 5% revenue decline from our estimates is more risky than a company that faces similar risk at 30% revenue decline scenario. (more…)

Neutral on Banking Sector – Nomura

Nomura of Japan has initiated coverage of the Indian banks sector with a NEUTRAL view. Key drivers of bank earnings – loan growth, interest rates (bond yields) and asset quality – have turned negative in 4QFY09 and are likely to deteriorate further in FY10E. Nomura expects earnings growth of Indian banks to drop 6% in FY10 after a robust CAGR of 21% over FY05-08. While banks are faced with these challenges, there is some comfort in state-owned banks’ valuations, which are trading at below book values, and fast-growing private banks, which are trading at 1-2x FY10E P/BV.

Nomura initiates a BUY on (more…)

Hindustan Zinc – Large reserves + low costs to Help

The recent sharp 33% qoq drop in zinc metal prices has led to a sharp cut-back in zinc mining output and led to a spate of mine closures. Cumulative reported mine closures have been to the order of 1.6 mn tons so far, which represent about 15% of global output. Zinc prices are expected to remain subdued in the near term owing to current surpluses and high inventories, we believe swift supply side response would help restore market equilibrium. (more…)

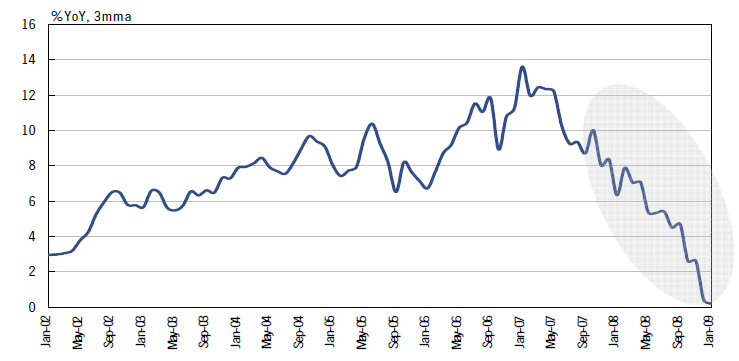

Historical Industrial Production Chart

We are presenting to you the Chart from our data that we have maintained over years about Indian Industrial Production Growth Rate.

Data from the following chart suggests that India’s IIP reported in Jan-09 is the lowest in the past 6 years.

Industrial Production – IIP Declines for Second Month in a Row

Industrial production declined 0.5% YoY in January-09 compared with a decline of 0.6% in December-08 (revised upwards from -2% earlier) and growth of 1.7% in November. The decline in January was lesser than market expectations (Bloomberg survey) of -0.9%.

The manufacturing segment declined 0.8% in January compared to -1% in the previous month. The key contributors to this decline were food products, non metallic mineral products, basic metal & alloy industries and metal products & parts. The mining segment also declined 0.4% in January compared to growth of 1.8% in the previous month. The growth in the electricity segment, however, accelerated to 1.8% vs. 1.6% in December.

Growth in consumer goods decelerated to 1.1% in January compared to 1.5% in December. Within consumer goods, growth in the durables segment accelerated to 2.5% on low base effect (vs. -4.1% in December) while non-durables segment growth slowed to 0.7% vs. 3% in December. Capital goods growth accelerated to 15.4% in January mainly on low base effect compared to 5.2% in the previous month. Basic and intermediate goods declined 1% and 9.2% in January (vs. +1.9% and -9.4% in December) .

Other indicators of activity such as the Purchasing Managers Index, exports growth, non-oil imports, and motor vehicle sales have also been very weak in January. We continue to expect activity to slow considerably in the January-March quarter of FY09.

In a related development, Indian Inflation Touched a new 6 year low at 2.43%.