American Financial Crisis, Historically High Oil Prices and the worst factor for Indian economy is Business Inflation – The rising cost of doing busines, together have all triggered the downgrading of Indian Equity Markets by Citigroup. In a report released just minutes ago, (more…)

American Financial Crisis, Historically High Oil Prices and the worst factor for Indian economy is Business Inflation – The rising cost of doing busines, together have all triggered the downgrading of Indian Equity Markets by Citigroup. In a report released just minutes ago, (more…)

Month: May 2008

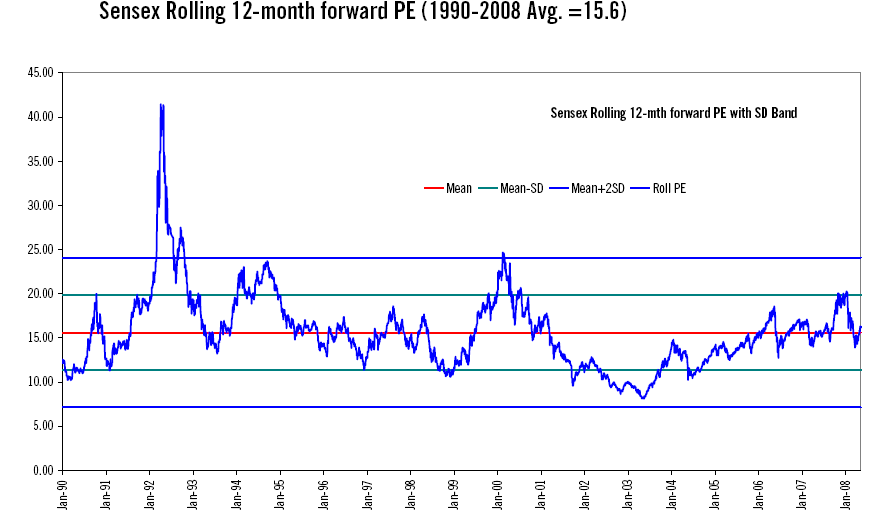

BSE Sensex – 1990 to 2008

This is the Best BSE Sensex historical graph I have ever seen and hence sharing it with you all. The Graph image can be enlarged to see Mean, Mean SD, Mean+ 2SD and Roll P/E. As the economy improved and the breadth of the markets increased, the SENSEX Rolling P/E has made lower peaks. 1992-93 peak was a result of Harshad Mehta Scam and 1999-2000 is Ketan Parekh + Sandeep Sabharwal IT Stocks Scandal [Inline with Global Dot Com Boom]

As the economy improved and the breadth of the markets increased, the SENSEX Rolling P/E has made lower peaks. 1992-93 peak was a result of Harshad Mehta Scam and 1999-2000 is Ketan Parekh + Sandeep Sabharwal IT Stocks Scandal [Inline with Global Dot Com Boom]

(more…)

Inflation at 7.61%

Inflation for the week ended Apr 26 comes at 7.61 % vs. market 7.57% for the week before. Inflation for the same period last year was 6.06%.

Inflation for the week ended Apr 26 comes at 7.61 % vs. market 7.57% for the week before. Inflation for the same period last year was 6.06%.

Late last week the price of Tea shot up by whopping 16% over the previous week. This week its rising again. Experts expect the Inflation to touch 7.68% for the week ending May 3rd 2008.

YTD Inflation for FY09 is at 7.41%. Morgan Stanley in its report has expressed concerns about India’s Macro scenario but however hasn’t downgraded India to a SELL yet 🙂

Inflation – Rising Cost of Doing Business in India

World’s leading banker, Citigroup has some harsh words for India in its report. Citi said,

World’s leading banker, Citigroup has some harsh words for India in its report. Citi said,

It has become expensive to live in India but probably even more expensive to do business in India. A look at the rising costs of setting up business over the last 3 years – asset, capital and services based – suggests “business inflation” could be as high as 10-35% p.a., well ahead of 7-8% headline inflation. This could be meaningful, given India’s growth is primarily investment led.

The report further adds that Business inflation is raising break-evens and capital intensity, lowering returns.

Citi estimates, ballpark by nature, suggest that in cases, break-even periods are up 20-80% over the last 3 years, capital intensity is up 10-60% and distribution requires 2x sales to generate the same returns. A part of this pressure is global, and this does not apply to all but raises questions on the direction of returns.

Citi raises 4 questions 1. Growth rates – where will they settle? 2. Government/RBI policy stance, in the face of inflation and election [frequent elections, a dampener] . 3. Earnings momentum – slowing, but faltering? 4. Retail investor – will he come back and when ?

Bartronics India – Going Strong

Bartronics India (BIL) reported an outstanding 495% yoy growth in its 4QFY2008 Top-line. This was a result of impressive growth in its Automatic Identification and Data Capture (AIDC) Solutions business, specifically in the RFID Solutions business, as also contribution from the Smart Cards segment. BIL had acquired a US company towards early 2008, which contributed Rs 33cr to Topline.

Bartronics India (BIL) reported an outstanding 495% yoy growth in its 4QFY2008 Top-line. This was a result of impressive growth in its Automatic Identification and Data Capture (AIDC) Solutions business, specifically in the RFID Solutions business, as also contribution from the Smart Cards segment. BIL had acquired a US company towards early 2008, which contributed Rs 33cr to Topline.

During 4QFY2008, BIL reported a 116bp yoy contraction in EBITDA Margins owing to higher operating costs viz., Raw Material, Staff Costs and Other Expenses. These expenses rose, as a % of Sales, by 675bp yoy, 19bp yoy and 179bp yoy respectively, in 4QFY2008. BIL’s total outstanding order book position at the end of FY2008 stood at a significant Rs345cr and constituted 128% of total FY2008 Revenues.

Kansai Nerolac Paints Outperformer – ICICI

Kansai Nerolac Paints’ Q4FY08 results were subdued due to lower demand for industrial paints [Automobiles]. Top-line grew 8.1% y-o-y to Rs 308.4 crore from Rs 285.2 crore. Bottom-line grew by a meagre 2.8% to Rs 24 crore from Rs 23.3 crore. Increase in realizations (2% in decorative segment) boosted EBITDA margin to 13.1% from 12.7% in Q4FY07. During the quarter, the company’s decorative business posted positive results as the housing segment continued to do well. (more…)

Kansai Nerolac Paints’ Q4FY08 results were subdued due to lower demand for industrial paints [Automobiles]. Top-line grew 8.1% y-o-y to Rs 308.4 crore from Rs 285.2 crore. Bottom-line grew by a meagre 2.8% to Rs 24 crore from Rs 23.3 crore. Increase in realizations (2% in decorative segment) boosted EBITDA margin to 13.1% from 12.7% in Q4FY07. During the quarter, the company’s decorative business posted positive results as the housing segment continued to do well. (more…)