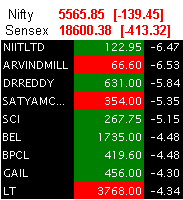

Satyam Computer Services net profit rose 28.58% to Rs 433.63 crore on 35.58% rise in total income to Rs 2266.05 crore in Q3 September 2007 over Q3 September 2006. The results are on a consolidated basis as per Indian GAAP.

Satyam Computer for fiscal 2008, under US GAAP, expects revenue between $2,119 million and $ 2,122 million, implying a growth rate of 45% to 45.2% over fiscal 2007. Basic earning per american depository shares (ADS) for fiscal 2008 is expected to be $ 1.27, implying a growth rate of 39.6% over fiscal 2007.

Corresponding revenue growth under Indian GAAP consolidated is expected to be between 29% and 29.2%. EPS for the full year is expected to be Rs 25.5, implying a growth rate of 18.9%.

For Q4 March 2008, under US GAAP, revenue is expected to be between $ 594 million and $ 597 million, implying a growth rate of 5.6% to 6.1%. Basic earning per ADS for the quarter is expected to be $ 0.36.

For Q4 March 2008, under Indian GAAP consolidated, corresponding revenue growth rate is expected to be between 5.3% and 5.8%; EPS for the quarter is expected to be between Rs 7.23.

Seperately, the company said it has entered into a definitive agreement to acquire Bridge Strategy Group, a Chicago based management consulting firm. In making the $35 million, all-cash purchase, Satyam significantly reinforces its strategy consulting and business transformation capabilities.